Buying a small business can be one of the fastest ways to become your own boss and build wealth. Many aspiring entrepreneurs search online for terms like “buy a business with no money down,” “seller financing,” or “zero down business acquisition.” While creative financing can sometimes help reduce the amount of cash needed, the reality is that buying a small business with zero money down is extremely rare. Most business sellers are not willing to offer seller financing with no down payment or only a very small down payment.

Why Sellers Want a Down Payment

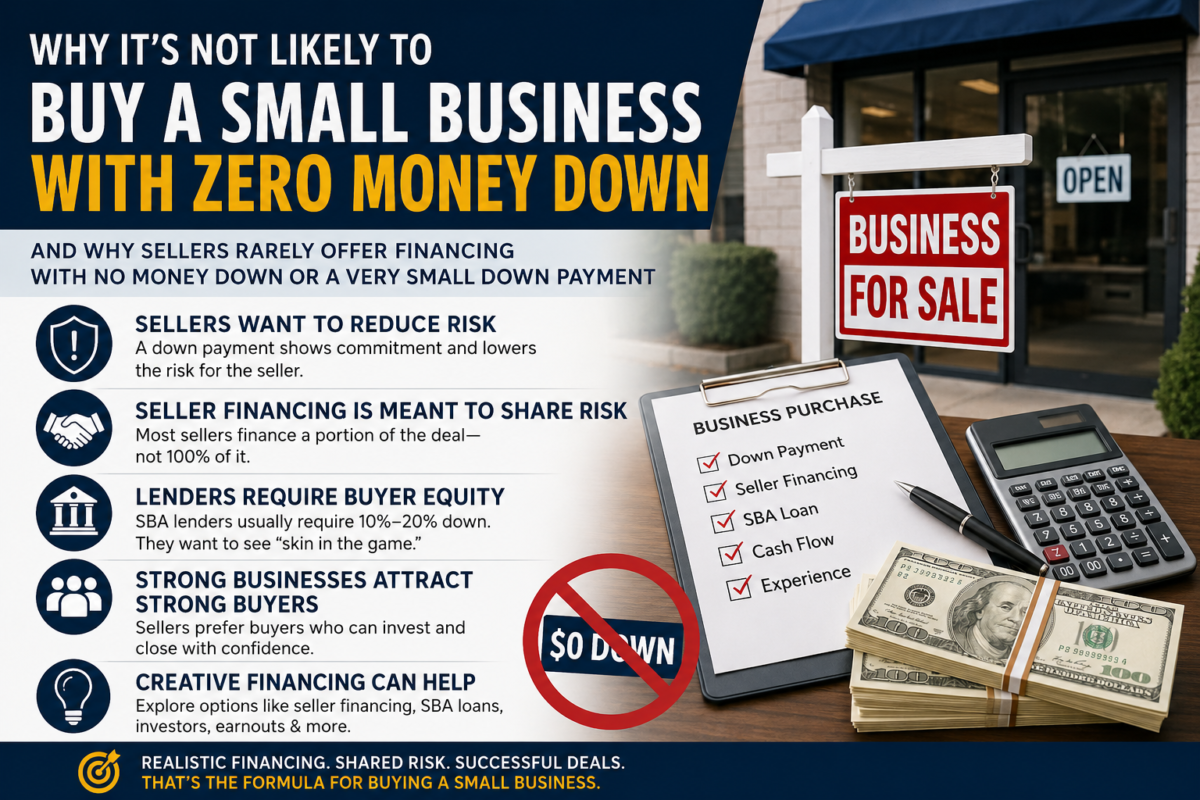

When a business owner decides to sell, they are usually looking to reduce risk and secure financial stability after years of hard work. A down payment demonstrates that the buyer has financial strength, commitment, and confidence in the business opportunity. Without a meaningful down payment, the seller assumes nearly all of the risk.

From the seller’s perspective, financing 100% of the purchase price means they are essentially giving the business away and hoping the buyer succeeds. If the buyer fails, the seller may lose both the business and the money owed. This is especially concerning in industries such as restaurants, retail stores, pharmacies, home health agencies, and service businesses where operations depend heavily on management experience and cash flow.

Seller Financing Is Meant to Share Risk

Seller financing is common in small business sales, but it is usually designed to share risk between buyer and seller — not eliminate it entirely. In many small business transactions, sellers may finance anywhere from 10% to 50% of the purchase price, depending on the strength of the business and the qualifications of the buyer.

A buyer who contributes a substantial down payment is more likely to remain motivated during difficult periods. Sellers understand that buyers with personal funds invested are generally less likely to walk away from the business if challenges arise.

For example, if a business is selling for $500,000, a seller may consider financing part of the deal if the buyer contributes $100,000 to $250,000 down. However, a request for zero money down often raises concerns about whether the buyer has adequate reserves, operating capital, or borrowing ability.

Banks and SBA Lenders Also Require Equity

Even when using SBA loans to buy a business, lenders typically require the buyer to invest their own capital into the transaction. SBA lenders want to see that the buyer has “skin in the game.” In many cases, SBA business acquisition loans require a 10% to 20% equity injection from the buyer, although structures can vary.

Lenders evaluate several factors, including:

- Buyer experience

- Credit history

- Industry background

- Available liquidity

- Business cash flow

- Collateral and guarantees

A buyer attempting to purchase a business with no money down may struggle to qualify for financing because lenders view the transaction as too risky.

Strong Businesses Attract Multiple Buyers

In today’s competitive business-for-sale market, quality businesses often receive multiple inquiries and offers. Sellers of profitable businesses in desirable locations usually prefer buyers who can close quickly and provide strong financial backing.

A seller comparing two offers will almost always favor the buyer offering a reasonable down payment over a buyer requesting 100% seller financing. Even if the financed offer is slightly higher, the reduced risk of a traditional structure is often more attractive.

Creative Financing Can Still Help

Although true zero-down deals are uncommon, creative financing strategies can still help buyers reduce upfront cash requirements. These may include:

- Partial seller financing

- SBA loans

- Investor partnerships

- Equipment financing

- Earnouts or performance-based payments

- Home equity lines of credit

The key is understanding that successful business acquisitions usually involve shared financial commitment from both parties.

If you are considering buying or selling a small business in Florida, working with an experienced business broker can help structure realistic financing terms and improve the likelihood of a successful closing.